API Holdings (PharmEasy) FY26 Deep Dive: From Billion-Rupee Losses to EBITDA Breakeven — And Why ₹6/Share Could Be a Historic Entry Point

Executive Summary

India's digital healthcare revolution has a new inflection point. API Holdings Limited — the unlisted parent entity of PharmEasy, Thyrocare, Ascent, and Aknamed — closed FY26 with its first-ever positive group-level EBITDA of ₹62.5 crore, reversing three consecutive years of deep operational losses. Revenue scaled 14.3% year-on-year to ₹6,869 crore, gross margins expanded meaningfully, and operating costs actually fell in absolute terms despite the revenue surge.

For pre-IPO investors watching from the sidelines, the question is no longer if API Holdings turns around — it already has, operationally. The question is when the full PBT-level profitability arrives, and whether the current unlisted share price of ₹6 per share adequately reflects the trajectory the business is now on.

This piece breaks down the numbers, the segment dynamics, the risks, and what it means for early-stage investors.

1. What Is API Holdings? Understanding the Business

API Holdings Limited is the holding company that sits above four distinct but interconnected healthcare businesses operating across India. Its portfolio spans pharmaceutical supply chain distribution, consumer healthcare delivery, hospital procurement, and diagnostics.

The four business units:

Ascent Health & Wellness Solutions (B2B Distribution): Supplies medicines to retail pharmacists and chemists across India. Retailers access the company's proprietary Order Management System (OMS). This is the revenue backbone of the group, contributing approximately 60% of consolidated revenue.

PharmEasy (B2C Consumer Platform): India's most recognized consumer health super-app. Facilitates home delivery of prescription medicines, OTC products, and diagnostics. Operated by Axelia Solutions Private Limited (an associate entity), while API Holdings retains the brand and technology. Historically loss-making due to customer acquisition and logistics costs, but now approaching breakeven.

Aknamed (Hospital B2B Supply Chain): Supplies pharmaceuticals, consumables, and surgical products to hospital networks. Undergoing active restructuring with significant cost-base reduction underway.

Thyrocare Technologies (Diagnostics): India's leading diagnostics chain, majority-owned by API Holdings (acquired in a ₹4,546 crore deal in 2021). The only profitable segment in the group — and the one carrying the entire portfolio financially at this stage.

In essence: B2B provides scale, PharmEasy provides consumer reach, and Thyrocare provides profit.

2. FY26 Group Financials: The Numbers That Matter

2.1 Revenue Growth

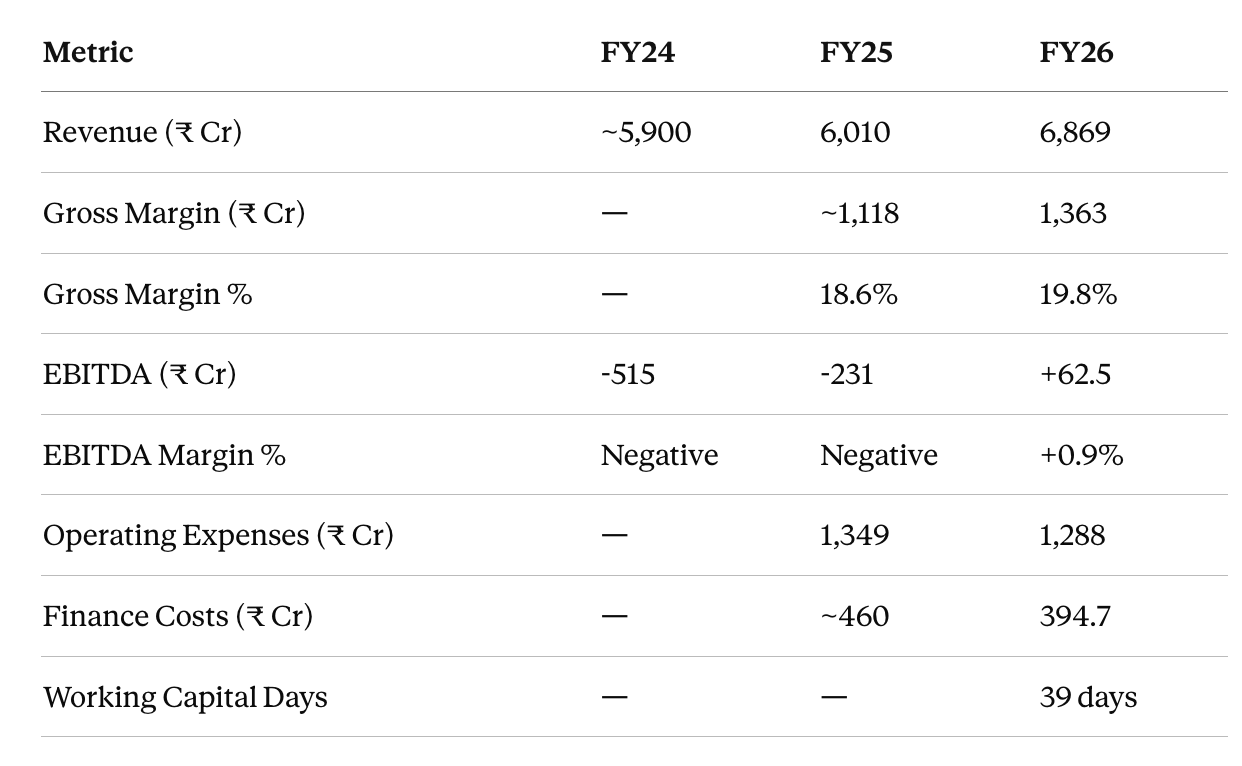

API Holdings posted consolidated FY26 revenue of ₹6,869 crore, growing 14.3% year-on-year from ₹6,010 crore in FY25. For context, the nine-month (9M FY26) figure had already reached approximately ₹5,095 crore — a 14.7% growth pace — before a strong Q4 pushed the full-year total higher.

Source: API Holdings Q4 FY26 Investor Presentation, May 2026. All figures in ₹ Crore.

2.2 The EBITDA Inflection

The single most important number in this analysis is the EBITDA trajectory:

FY24: ₹515 crore EBITDA loss

FY25: ₹231 crore EBITDA loss

FY26: ₹62.5 crore EBITDA profit

This is a ₹577 crore swing in EBITDA over two years, driven by two simultaneous forces. Gross margins expanded 130 basis points — from 18.6% to 19.8% — reflecting better product mix and procurement efficiency. Simultaneously, operating expenditure as a percentage of revenue fell 370 basis points, from 22.4% to 18.7%. In absolute terms, opex fell from ₹1,349 crore to ₹1,288 crore even as revenue grew by ₹859 crore. That is textbook operating leverage.

2.3 What Still Weighs on Profitability

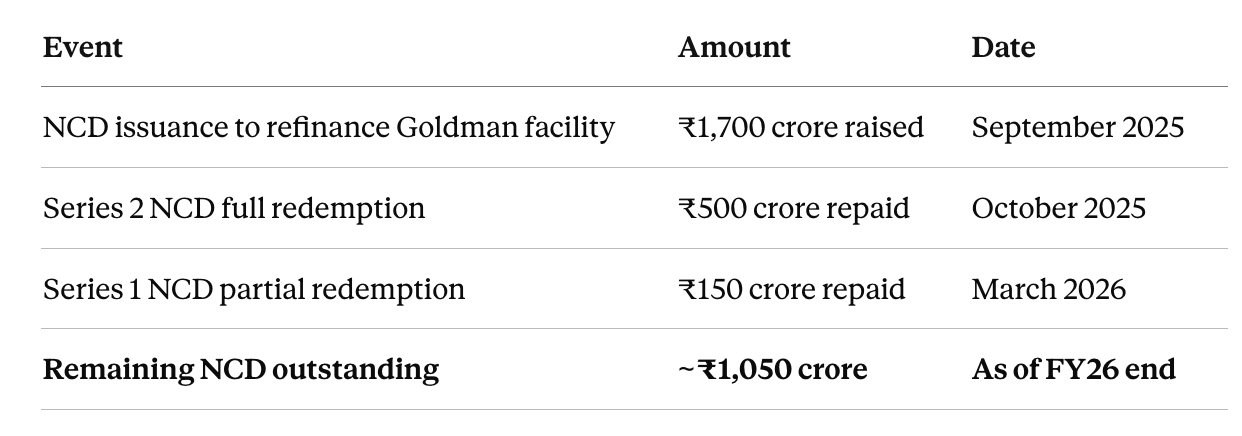

While EBITDA has turned positive, the Pre-Tax Profit (PBT) remains negative at approximately -₹388 crore. Finance costs — the legacy of the debt-funded Thyrocare acquisition in 2021 — still account for ₹394.7 crore annually. This is down sharply from approximately -₹2,300 crore PBT in FY24, but debt remains the primary barrier to net profitability.

The NCD debt outstanding stands at approximately ₹1,050 crore as of end-FY26, following partial redemptions: ₹500 crore in NCDs were fully redeemed in October 2025, and a further ₹150 crore partial redemption was made on 30 March 2026. The debt reduction trajectory is now clearly established.

3. Segment Deep Dive

3.1 B2B Distribution (Ascent) — The Revenue Engine

FY26 Highlights:

Contributes ~60% of group revenue

Revenue grew ₹535 crore year-on-year

Operating expenditure fell ₹45 crore despite the revenue increase

Q4 FY26 EBITDA reached ₹16.9 crore at 1.6% margin — the highest quarterly figure on record

Working capital improved from 53 days to 44 days

The B2B segment achieved its first EBITDA breakeven at ₹1.3 crore for the full year — a landmark milestone for a segment that has historically generated razor-thin margins. The Q4 momentum at 1.6% EBITDA margin suggests FY27 could see sustained positive contributions from this segment.

Key risk: Gross margins remain thin at approximately 9%, leaving limited cushion against procurement price volatility.

3.2 PharmEasy (B2C) — The Great Narrowing

FY26 Highlights:

Gross margin expanded sharply from 22.8% to 25.7% (approximately 27% in Q4 alone)

Full-year EBITDA loss narrowed from -₹86.1 crore (FY25) to -₹39.4 crore (FY26) — a 54% improvement

Q1 FY26 EBITDA loss: -₹21.1 crore; Q4 FY26: -₹5.2 crore — a dramatic quarterly improvement

Q4 EBITDA margin at -1.5%, approaching breakeven

The PharmEasy story in FY26 is one of disciplined margin expansion. Operating losses more than halved, gross margins hit a new high, and Q4 came within 1.5 percentage points of operational breakeven.

One caution: opex grew 10.9% year-on-year (₹344 crore to ₹382 crore), indicating continued investment in marketing or last-mile delivery. Whether this spending translates into sustained market share gains will determine the FY27 EBITDA breakeven timeline.

Why this matters for valuation: The PharmEasy re-IPO narrative — which was derailed post-2022 — fundamentally depends on EBITDA breakeven. Every quarter closer to that milestone is a potential re-rating event for the unlisted holding company.

3.3 Aknamed — Restructuring in Progress

FY26 Highlights:

Revenue declined approximately 2% year-on-year — the only segment to post a revenue decline

Opex collapsed 64.1% from ₹141.7 crore to ₹50.9 crore (primarily due to reversal of Expected Credit Loss provisions)

Working capital days remain elevated at 80 days — the highest across all segments

Aknamed is the most complex part of the portfolio. The headline opex reduction is impressive but largely driven by the reversal of ₹187.5 crore in FY24 Expected Credit Loss provisions — a non-recurring item. Gross margins have compressed steadily from 8.2% (FY24) to 5.5% (FY26), and Q4 FY26 EBITDA deteriorated to -4.9% after a near-breakeven Q3 (-0.4%).

The segment requires strategic attention: either revenue growth to offset the thin margin structure, or further cost rationalisation.

3.4 Thyrocare — The Profit Powerhouse

FY26 Highlights:

Consolidated revenue grew 21% year-on-year to ₹829 crore

EBITDA grew 38% year-on-year to ₹262 crore (EBITDA margin: ~31.6%)

Group-reported Thyrocare EBITDA contribution: ₹279.9 crore at 33.8% margin

Profit After Tax surged 81% to ₹162.85 crore

Q4 FY26 PAT jumped 128% year-on-year to ₹48.7 crore

Total test volumes rose 23% year-on-year to 209.6 million in FY26

Q4 EBITDA margin hit 35.1% — a new quarterly record

Thyrocare is the financial anchor that makes the API Holdings story viable. At ₹279.9 crore of EBITDA contribution, it alone generates more profit than the combined losses from PharmEasy and Aknamed (approximately ₹53.3 crore combined). The segment is expanding into high-margin specialty diagnostics: genomics, advanced allergy testing (250+ SKUs on the Phadia platform), and Non-invasive Pre-Natal Testing (NIPT).

For perspective, Thyrocare is a listed entity trading on Indian exchanges at meaningful valuation multiples — and it represents the largest single source of intrinsic value within the unlisted API Holdings structure.

4. Debt Trajectory: The Critical Remaining Overhang

The Goldman Sachs facility of ₹2,700 crore — originally raised in May 2022 to finance the Thyrocare acquisition — has been the defining financial constraint on API Holdings since 2022. The refinancing and repayment journey is now well underway:

Sources: Outlook Business (September 2025); Elite Wealth (November 2025); Exchange filings (March 2026)

The Thyrocare share pledge (approximately 60.93% of equity, held by subsidiary Docon Technologies) remains in place as collateral against the outstanding NCDs. As debt reduces, this pledge overhang diminishes — and with it, one of the primary risk factors for the unlisted company.

Finance costs fell from approximately ₹460 crore in FY25 to ₹394.7 crore in FY26. If the ₹1,050 crore NCD balance is repaid over FY27–28 (likely using a mix of Thyrocare dividend income, operating cash flows, and potential asset monetisation), finance costs could fall to under ₹150 crore — turning the PBT line from negative to positive.

5. Operational Improvements: Beyond the P&L

The FY26 results reveal several qualitative improvements that do not fully show up in headline numbers:

Working capital discipline: Group-level working capital improved from approximately 50 days (9M FY25) to 39 days (FY26), freeing meaningful cash from operations. B2B alone improved from 54 to 44 days.

Management transition: In August 2025, co-founder Siddharth Shah stepped back from the CEO role, with Thyrocare's MD & CEO Rahul Guha elevated to lead the group. The transition brought a more operationally grounded leadership style to the company at a critical juncture.

Cost culture shift: The group has moved decisively from a growth-at-any-cost model (which characterised the 2020–2022 expansion phase) to an efficiency-led framework. The combination of rising revenue and falling absolute opex in the same year is the clearest evidence of this shift.

6. The IPO Question

API Holdings originally filed its Draft Red Herring Prospectus (DRHP) with SEBI in late 2021, targeting a ₹6,250 crore IPO. SEBI approved the filing, but the company withdrew plans amid market volatility, governance concerns, and deteriorating financial metrics.

The re-IPO narrative is back — but this time with a fundamentally different financial profile. The key milestones the market will watch:

PharmEasy EBITDA breakeven (FY27): The most critical single trigger. At Q4 FY26's -1.5% EBITDA margin, this is within reach.

PBT turning positive: Dependent on continued debt reduction and finance cost decline.

Aknamed stabilisation: Needs to reverse gross margin compression and resolve elevated working capital.

Thyrocare sustaining 30%+ EBITDA margins: The foundation of any IPO valuation story.

If PharmEasy achieves EBITDA breakeven in FY27 and debt falls to ₹500–700 crore range, the group-level PBT could turn positive — at which point the IPO valuation conversation changes materially.

7. Valuation Context: What Does ₹6/Share Actually Imply?

At the current unlisted share price of ₹6 per share, API Holdings is trading at a deep discount to the sum-of-parts value of its portfolio.

Consider just the Thyrocare component: listed on exchanges with a market capitalisation reflecting strong FY26 financials (81% PAT growth, 21% revenue growth), API Holdings' ~61% economic stake in Thyrocare alone represents substantial value. The remaining businesses — B2C, B2B, and Aknamed — come at a fraction of that, despite showing clear operational improvement.

Pre-IPO investments in companies on EBITDA inflection trajectories have historically generated significant returns when the IPO does materialize. The current price reflects the risk premium associated with legacy debt, PBT-level losses, and the uncertainty around IPO timing — not the operational reality of where the business is heading.

Key parameters for investors to track:

Quarterly EBITDA trajectory of PharmEasy (watch for FY27 breakeven)

Rate of NCD debt repayment

Thyrocare quarterly performance (the compounding anchor)

Any IPO-related announcements or DRHP re-filing

8. Risk Factors

Investing in unlisted, pre-IPO shares carries materially higher risk than investing in listed securities. Specific risks for API Holdings include:

Balance sheet risk: ₹1,050 crore in NCD debt with Thyrocare shares pledged as collateral. Any sustained decline in Thyrocare's listed share price could tighten collateral requirements.

Aknamed structural concerns: Gross margin compression (8.2% → 5.5% over two years) and 80-day working capital cycle indicate potential collections and profitability risk in the hospital supply chain business.

PharmEasy execution risk: EBITDA breakeven in FY27 is not guaranteed. A relapse in opex discipline or competitive pressure on margins (from players like 1mg/Tata Health, Netmeds/Reliance) could delay the timeline.

IPO timeline uncertainty: There is no confirmed date for re-filing or listing. Unlisted share investors have no guaranteed liquidity event.

Concentration risk: Thyrocare's profitability is carrying the group. Any deterioration in diagnostics sector dynamics would disproportionately impact API Holdings.

9. Conclusion: A Turnaround That Is Already Happening

The API Holdings story in FY26 is not about potential — it is about execution. The group has delivered:

A ₹577 crore swing in EBITDA over two years

14.3% revenue growth to ₹6,869 crore

Gross margin expansion from 18.6% to 19.8%

Opex reduction in absolute terms despite growing revenue

₹650+ crore in debt repaid since the Goldman Sachs refinancing

Thyrocare PAT growing 81% with Q4 margins at a record 35.1%

PharmEasy losses narrowing from -₹86 crore to -₹39 crore in a single year

The business still carries legacy financial burdens — primarily the ₹1,050 crore NCD balance and resulting finance costs. But the operational engine is clearly running better, and the direction of travel is unambiguous.

At ₹6 per share, the market is pricing in the risks but arguably not fully pricing in the trajectory. For investors with a 2–4 year horizon, appetite for pre-IPO risk, and conviction in India's healthcare digitisation story, API Holdings represents one of the more interesting unlisted opportunities in the Indian healthcare space today.

Interested in Purchasing API Holdings (PharmEasy) Unlisted Shares at ₹6/Share?

Valowth Capital facilitates access to API Holdings unlisted shares at the current market price of ₹6 per share.

To enquire, check availability, or initiate a purchase, connect with our team directly on WhatsApp:

👉 [Click here to connect on WhatsApp]( http://bit.ly/4ubvsfM )

Our team typically responds within a few hours during business hours.